(Photo: Flickr / Marco Verch)

(Photo: Flickr / Marco Verch) It is pensioners rather than all investors, who are being really hammered right now. When you save money towards a long-term goal, such as retirement, you can endure dips such as Covid-19 and the 2008 subprime lending crisis.

One of the advantages of market dips, when you are building up savings on a regular basis, is that you are buying cheap assets that will gain value as markets improve again.

But when you retire and live on an income, based on your retirement savings, it’s very different. When you are drawing down income, you are reducing your capital at a far greater rate when investment markets collapse.

The pensioners, who are facing the greatest dangers, are those who are using investment-linked living annuities (Illas). And 90% of all pensioners choose this investment vehicle rather than the traditional life assurance guaranteed annuities (pensions).

Let’s say today, no matter how long you have been retired, you have retirement capital of R6-million. You are drawing down 7% of your capital a year, giving you R35,000 a month. (Be warned: At an average of 7%, pensioners are already in trouble, but it is the reality of how things are in South Africa).

The market then crashes by 20%, reducing your capital to R4.8-million. You stick to your R35,000 a month (R420,000 a year), because you can’t afford to live on less and you can only change the income levels on your annual anniversary date. This means that you are now withdrawing at a rate of 8,75%, but if we take inflation at 5%, your actual withdrawal is now a withdrawal of 13.75%. Your after-inflation capital is now worth R4,140,000

The following year markets level out, but do not recover and you continue to withdraw the same amount of R35,000.

In the third year, your capital has now reduced to R3.96-million and your drawdown is now at 10.66%.

By the end of year nine, you have reached your maximum drawdown of 17,5%. You have reached what is called the “point of ruin” where your income will drop in real terms and that is before inflation. In buying terms, because of inflation, your buying power reduced a few years earlier.

The problem now is that you will never know when investment markets will recover. For example, in nominal terms without inflation, the New York Stock Exchange took until 1952 to recover from the great depression of 1929; and Japan which reached the dizzy height of 30,000 in 1992 is still nowhere near that mark 29 years later.

The effects are likely to be more devastating for the South African economy. Around the world, we are seeing a far wider reach of problems related to Covid-19 than the property burndown.

Unlike 2008, we now have almost every industry involved, particularly in countries that are in virtual lockdown. For example, in 2008 shops, theatres and restaurants stayed open, and people were allowed to travel, but this is not the case with the Covid-19 crisis.

I strongly suspect that the investment market will take longer to recover this time as well.

But they should recover, particularly in countries that have cash on hand, such as western developed economies.

However, in South Africa, particularly after the National State of Disaster was declared by President Cyril Ramaphosa, recovery will be slower because the country is already desperately short of funds and is faced with the fallout of years of extensive fraud and corruption.

Then we have the Saudi Arabian and Russian fuel war, which has already shrunk the oil price internationally, and hit Sasol, a major contributor to the economy, reducing its share price by 95%.

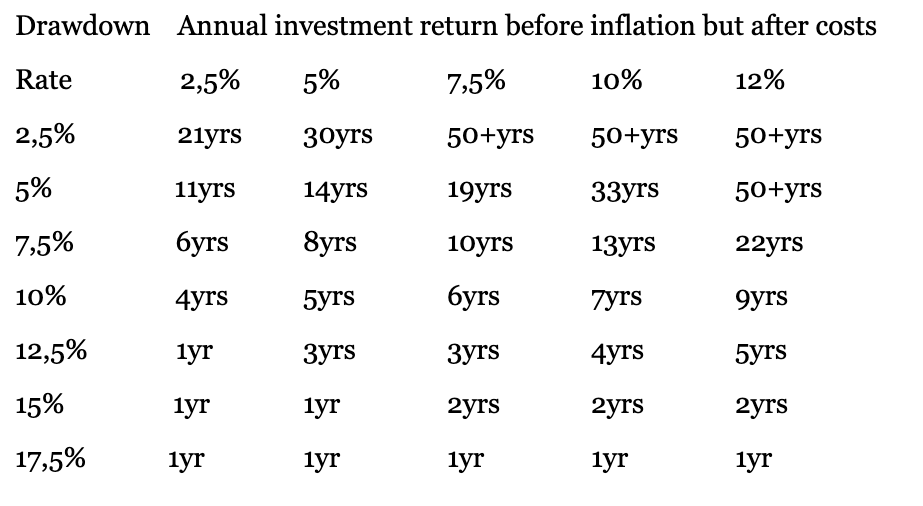

Now let’s look at the proposed industry drawdown for pensioners proposed by the industry body, the Association for Savings and Investment South Africa (Asisa), and the draft proposals by the regulator, the Financial Sector Conduct Authority (FSCA) for a Standard for Illas relating to default annuities offered by retirement funds.

Asisa has a table that shows how long your income is likely to last before you hit the “point of ruin”:

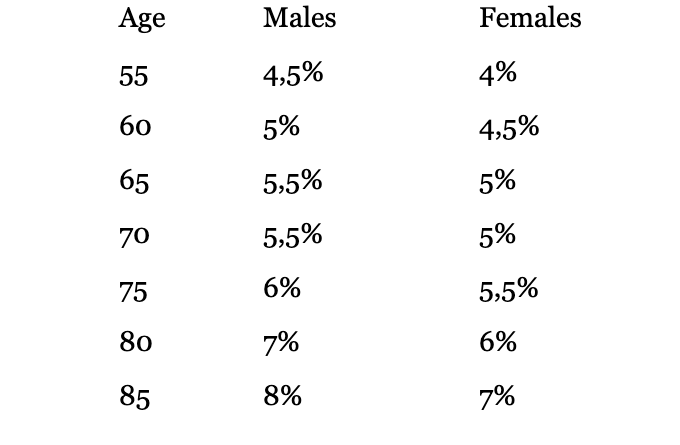

FSCA recommends the following draft maximum drawdown rates by age should be:

Now look at your expected average age of death. According to figures of the Actuarial Society of South Africa, any female who reaches age 60 can be expected to live until 84; and any male at age 60 can be expected to live until age 79. For a couple aged 60, there is a 50% chance that at least one of them will still be alive at age 90. But these are averages – a lot of pensioners will live beyond these averages.

On the Asisa tables, assuming an initial investment return of between 2.5% and 5%, only females with a drawdown rate of 3.44% (at most) can expect to live virtually free of the “point of ruin”; and only males with a drawdown rate of 4.22 (at most) can live past the “point of return”. Any higher initial drawdown will lead to ruin.

But these tables are likely to be on the optimistic side. There is a lot of research both here and overseas that at age 60, your drawdown rate should not be above 4%.

The problem is that many South Africa Illa pensioners are already in serious trouble. At an average drawdown, as reported by Asisa, of 7%, pensioners are already beyond their limit.

Another problem is the average structure reported by Asisa on its members. In the reporting, the pensioners are weighted by the amount of capital they have, thereby generally understating the drawdown rate if one were to determine it by numbers of pensioners. In addition, the average figures don’t show which pensioner groups are most vulnerable.

The richer people, of which there are few, make up the money weight on the upside of the averages, because they have lower drawdowns, often as low as 2.5% and then many will also reinvest these; while medium to lower income people, who make up the numbers, are on the lower side, drawing far more than the 7% average.

So while you have one pensioner below the 7% drawdown, you will have 10 pensioners drawing down far more than 7%.

Recent research by Alexander Forbes, based on the retirement funds it administers, show that many pensioners were already in serious trouble before Covid-19 – the virus and the resulting investment market downturn just makes it a lot worse.

An actuary and a leader in retirement research, John Anderson, Alexander Forbes head of strategic development, says many South African pensioners are in a bad way already because of decisions they made as far back as 20 years ago when they retired – and this is apart from most pensioners saving too little when they built up their savings when they were still employed.

Covid-19 is going to see many more pensioners hit the “point of ruin” far more quickly. BM

Over the following weeks, a series of reports written by Bruce Cameron, the semi-retired founding editor of Personal Finance of Independent Newspapers, will look at the effects of Covid-19 and research undertaken by Alexander Forbes on retirement income in South Africa.