The pricing of Saudi Arabian Oil Co., or Saudi Aramco, can best be summed up with the headline “World’s Biggest Dog Bites World’s Biggest Man.” Shares sold at 32 riyals ($8.53) apiece, at the top of the range of 30-32. Combine that extraordinarily narrow range with the lack of a global offering, a stake being sold of just 1.5% and inducements including bonus shares and guaranteed dividends, however, and anything less than the maximum would have been astounding. As it is, having raised at least $25.6 billion, the Saudi government obtains #biggestIPOeva bragging rights. In terms of maximizing proceeds or setting a credible price on the family silver, not so much.

Still, at least doing it this way — along with the interesting choice on timing — meant the (interminable) festivities in Vienna wouldn’t have any impact on Thursday. The same can’t be said for what happens from here.

As of 10.30 p.m. in Vienna, the OPEC meeting was still going on, and the usual press conference had been postponed to Friday. This is not a good sign. The broad outline of a plan seemed to be emerging on Thursday, with OPEC+ set to raise its supply cuts from the current level of about 1.2 million barrels a day to just under 1.7 million barrels a day.

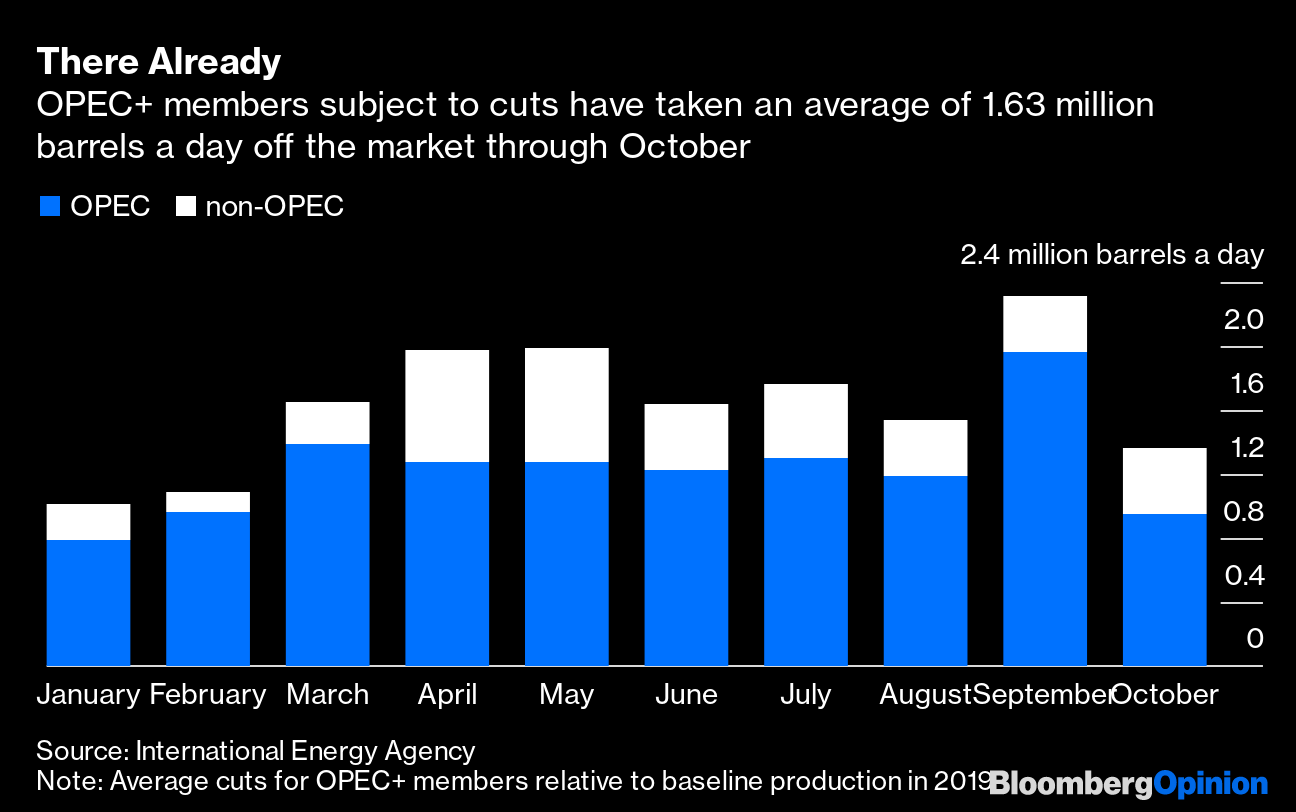

That begins to get at the problem. Because, in the year-to-date through October, cuts have averaged … just under 1.7 million barrels a day.

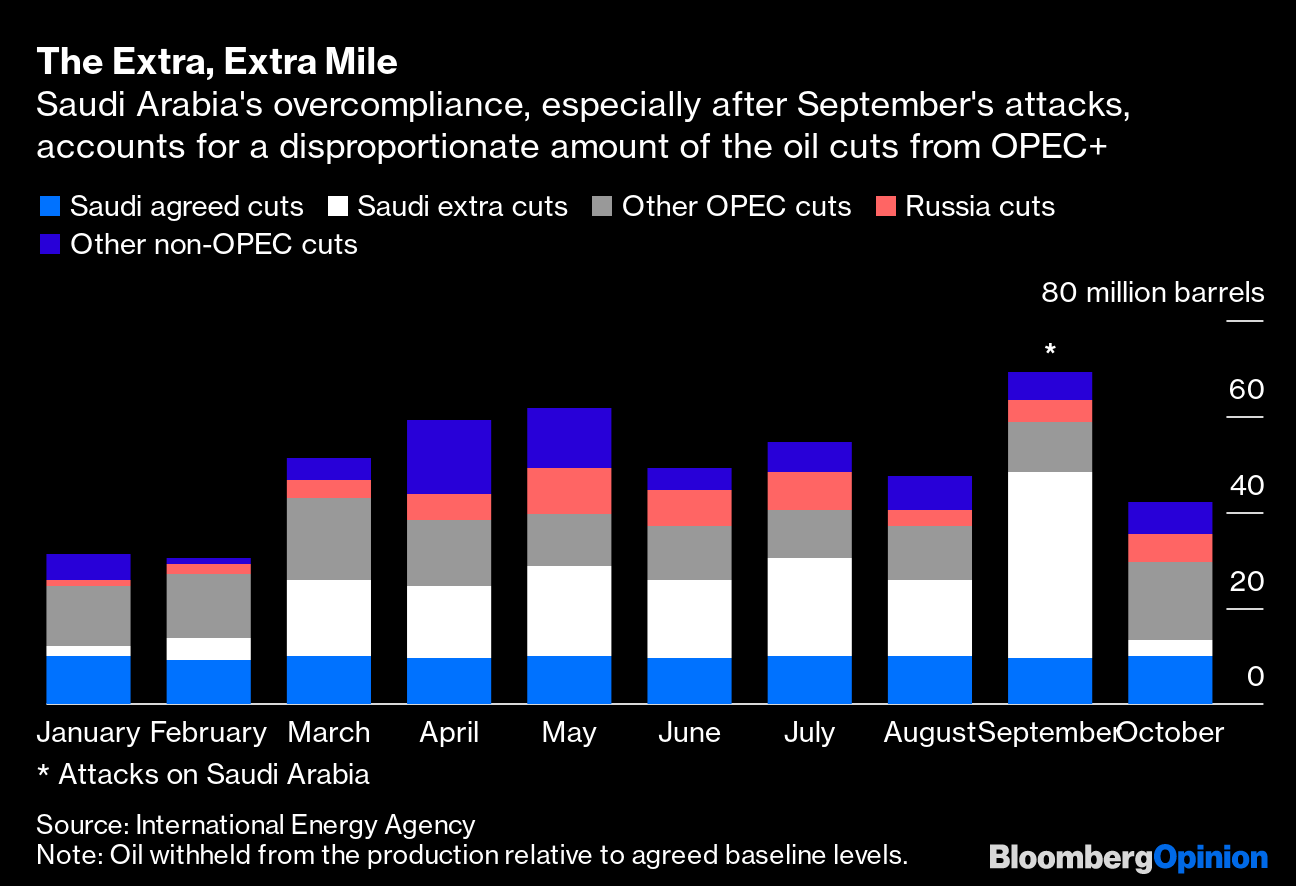

Beneath that broad over-compliance, though, a handful of high-achievers do most of the work. Of the OPEC members of any size, only Angola, Kuwait and Saudi Arabia complied in every month of this year through October. On the non-OPEC side, keystone country Russia managed that for just three months, and then mainly due to contamination problems. Saudi Arabia is doing the heavy lifting here, accounting for less than a quarter of baseline production but fully half the barrels OPEC+ kept off the market — and not always by choice.

The new cut, therefore, looks more like an attempt at rebalancing — which would explain the extended in Vienna. Apportioning the extra cuts on a pro-rata basis would effectively let Saudi Arabia keep pumping at October’s level, which is actually 4% higher than its average for the year. Of the other major producers, it would mostly penalize Iraq and Russia.

Already, though, Russia’s position is clouded by a debate over whether its production of condensate — gaseous hydrocarbons that turn to liquid at the surface — should be excluded from its agreement. There’s a legitimate argument there, as OPEC members don’t include condensate in their targets. In practice, it would create more wiggle room for a habitual wiggler. As for Iraq, it looks back on decades of disruption from multiple wars and sanctions and feels justified in catching up (it is also distracted with bigger problems at home right now).

In theory, Saudi Arabia can threaten to open the taps, and maybe it should. Doing so would hit the ranks of U.S. tight-oil producers, full of walking wounded already. In terms of maximizing the long-term value of Saudi Arabia’s reserves — and Aramco’s valuation — knocking out some competitors and encouraging demand makes sense. But there would be no hiding the short-term damage inflicted on Aramco’s financials. All else equal, based on my math, the extra free cash flow generated by boosting output from 10 million barrels a day to 10.5 million would be wiped out by just a $3 drop in oil prices — and they likely would drop by much more if Saudi Arabia tried to flush the market.

As it stands, even if the “cuts” are agreed, they’re unlikely to, well, cut it. OPEC crude oil production was 29.7 million barrels a day in November, according to Bloomberg estimates. Current estimates from the likes of OPEC itself and the IEA suggest the amount of oil required from the group to balance the market through the first half of 2020 ranges from about 28 to 29 million barrels a day. Even a real extra cut of 500,000 barrels a day looks inadequate to prevent a new-year price drop.

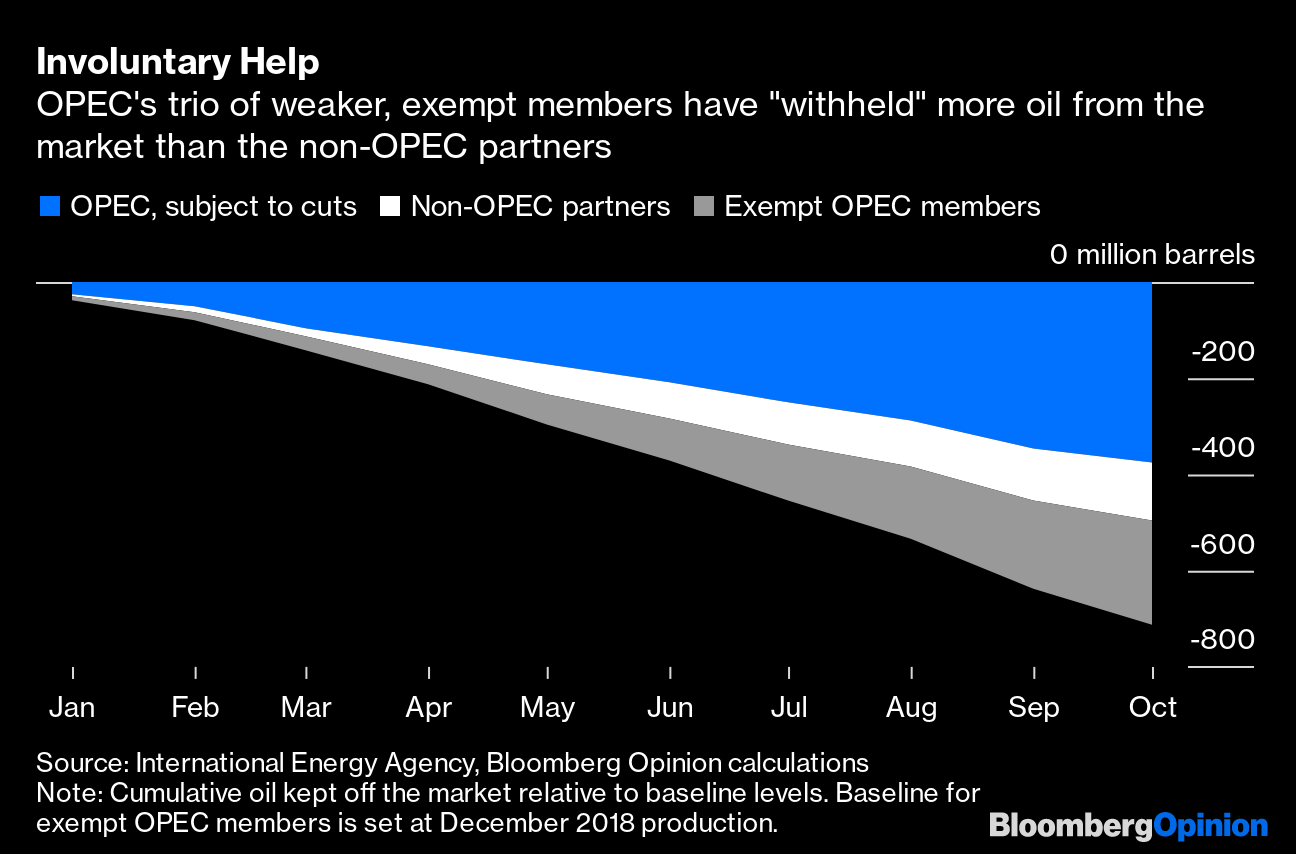

It is also worth bearing in mind that, while OPEC+ has shown notable discipline as a whole, it continues to benefit enormously from the weakness of three members who aren’t even subject to caps. Last December, Iran, Libya and Venezuela produced a collective 5.1 million barrels a day of crude. Using that as an ersatz baseline, the continuing drop in their output “contributed” 217 million barrels staying off the market through October — almost double the amount withheld by Russia et al.

Above all, despite more than 600 million barrels being held off the market through the end of September, commercial oil stocks in the OECD countries actually increased slightly during that time (and that doesn’t include China’s continued stockpiling).

Whatever Friday brings, it has been apparent since OPEC+ began this six-month program three years ago that its grip has slipped. As if to reinforce that, Aramco’s mega-IPO finally priced, but on notably narrow terms. The headlines are bold and the drama remains. But the forces at work in today’s oil market simply can’t be managed from an office in Vienna.

DM