Fast forward to December 2019, and we have President Donald Trump’s latest furious denunciation of exactly the same thing — only this time, he says that Brazil (as well as Argentina) is being unfair. In his latest tweet heard around the world, he said: “Brazil and Argentina have been presiding over a massive devaluation of their currencies. which is not good for our farmers.”

After announcing the imposition of tariffs on Brazilian and Argentine steel, he went on to attack the Fed. He wants the central bank to return to the behavior that so annoyed Mantega a decade ago: “The Federal Reserve should likewise act so that countries, of which there are many, no longer take advantage of our strong dollar by further devaluing their currencies. This makes it very hard for our manufactures & farmers to fairly export their goods. Lower Rates & Loosen - Fed!”

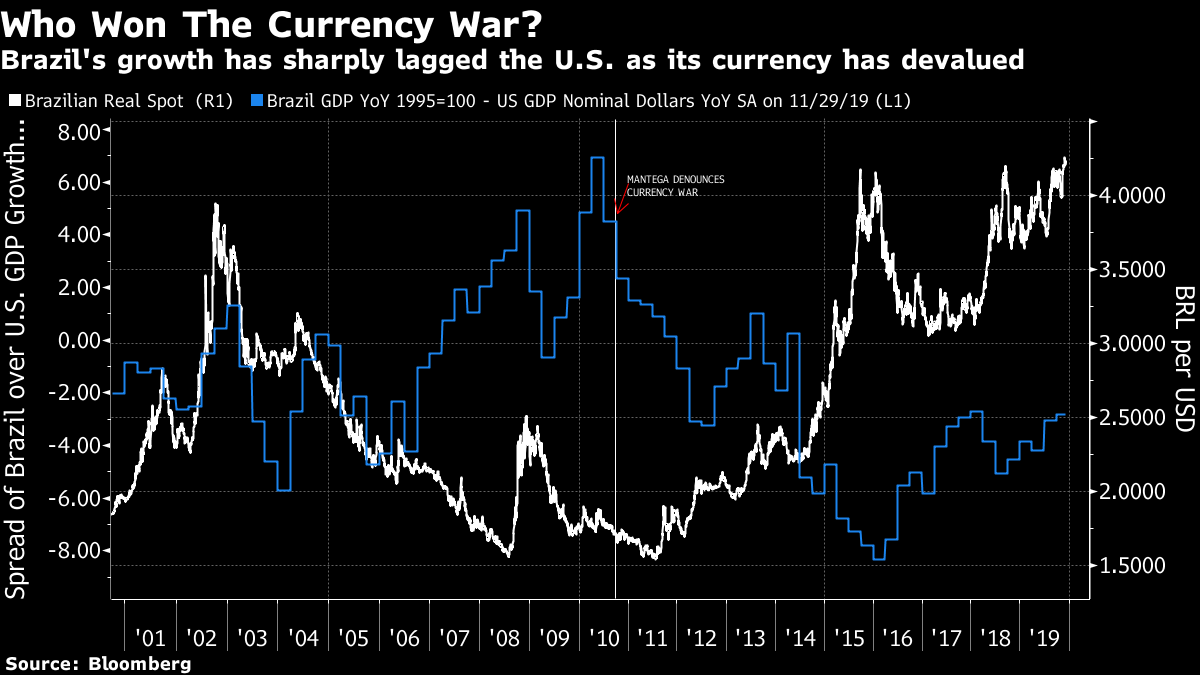

If Mantega’s complaints look dumb in retrospect, Trump’s latest broadside looks even dumber. Mantega’s complaint came when Brazil’s economy was surging on the back of strong commodity prices (which themselves were driven by the voracious manufacturing appetite of China). The strong Brazilian real hadn’t stopped the country’s economy from going on a great run. In the subsequent decade, the U.S. far outstripped Brazil’s growth, despite a steadily strengthening dollar:

Currency values matter greatly to competitiveness, of course, and central banks can use interest rates to manipulate them. But the arrow of causation also works in the other direction. A weak economy will lead to a weak currency, and vice versa. That is the story of the U.S. dollar and the Brazilian real over the last decade.

The weak dollar in 2010 was a product of the weakness of the U.S. economy. Low rates and quantitative easing were deemed necessary to keep the economy ticking over, and allow the country to clear its debts. Outright deflation appeared a real risk. Higher rates from the Fed at that point might have weakened the real, but they might also have stopped U.S. economic growth in its tracks — which would have been very bad news for Brazil.

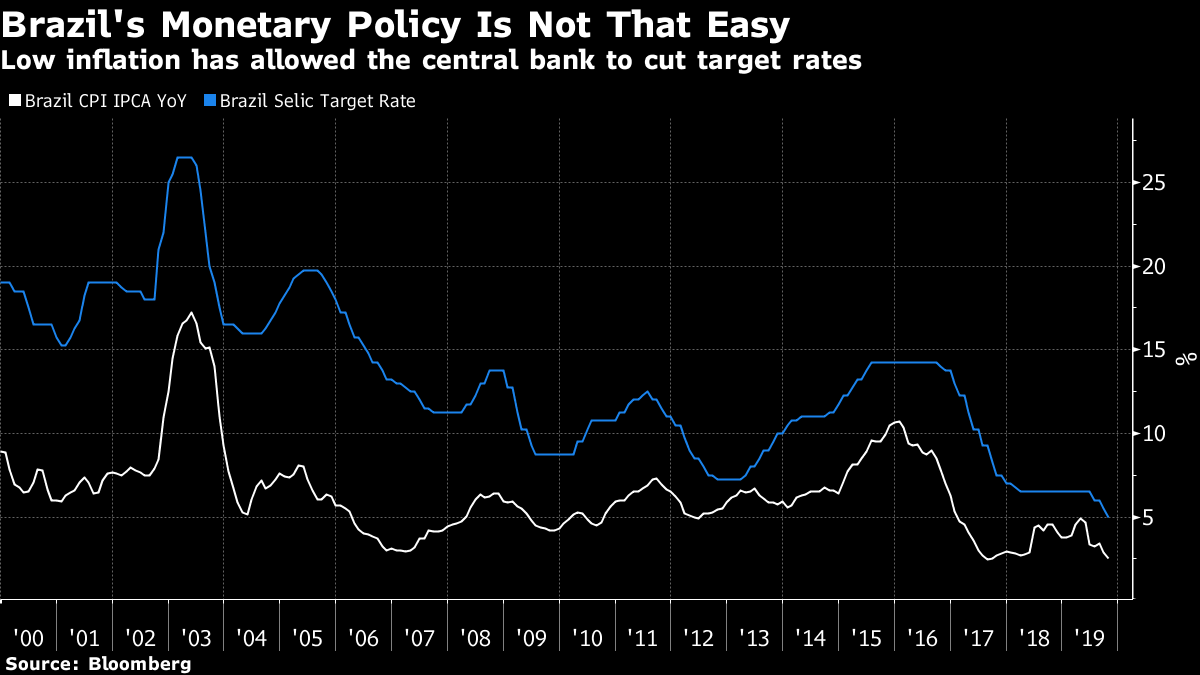

Is Brazil manipulating its currency lower? Not at all. Its central bank’s target rate, the Selic, is very low at present, by Brazilian standards, but only because inflation is at its lowest this century:

Further, asthe country’s use of dollar-denominated debt has increased over the last decade, a weak real makes interest payments more expensive and increases the risk of a crisis.

No country knows this better than Argentina, which has suffered several epic crises of devaluation and default in living memory, and where voters have just kicked out a president, Mauricio Macri, in large part for failing to tame inflation. Macri failed to stop further sharp devaluations of the Argentine peso, despite massive overnight rates of more than 50%. Another disadvantage of a weak currency is inflation, and Argentines know all about that. It too is currently running at more than 50%. Any implication that Argentina is deliberately weakening its currency for competitive advantage is beyond absurdity.

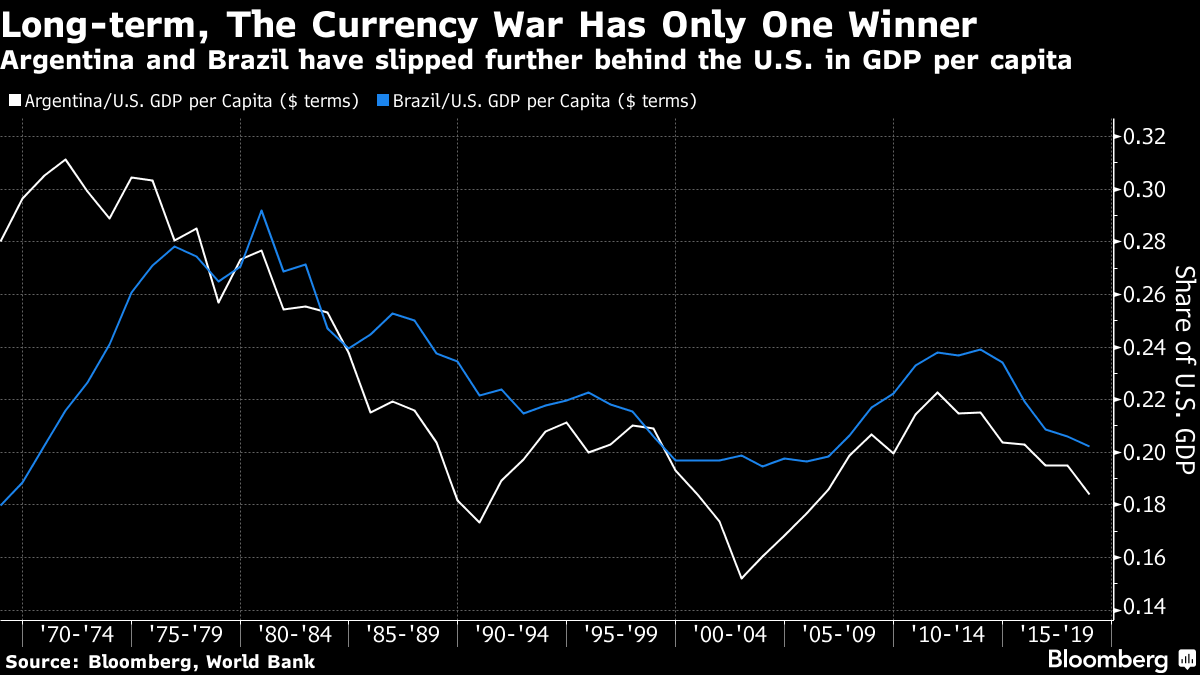

In the long run, the currency war has had only one winner. GDP per capita in both Brazil and Argentina is less than a quarter that of the U.S. And both countries have fallen further behind, even as their currencies have weakened.

Why, then, is Trump choosing to open a new front in the trade war, on two countries that currently have little or no ability to harm the U.S.? It is possible that he is being “crazy like a fox,” and trying to convince people that he is capable of anything. Such a strategy, the argument goes, might convince China of the need to do what he wants. The risk with such a strategy is to give the appearance that he has no understanding of how the economy works. And thus the more likely explanation for his behavior is that he truly doesn’t understand what he is doing.

Meanwhile, Brazil and Argentina have shown the U.S. the best way to weaken a currency. If your economy slows down, the chances are that your currency will get cheaper. That is what has happened over the last decade to the big economies of South America. And in the much shorter term, the sharp sell-off in the dollar on Monday in response to disappointing data on manufacturing suggests that the president should be careful what he wishes for. Today’s weak Brazilian real appears to be exactly what Guido Mantega wished for back in 2010 — but nobody in Brazil could possibly have wished for the disastrous decade that made that weak currency possible.

DM