Vodacom: still reliant on the domestic market

Interim results show Vodacom Group’s revenue has increased by 4.3% and EBITDA (Earnings Before Interest Tax Depreciation and Amortization) by 2.4% when compared to last year’s same six-month period. The group’s customer base has increased 5.8% over the period to 110 million.

Revenue growth continues to be led by international data sales which increased by more than 25% in the six-month reporting period. However, international data revenue accounts for only 11% of group data revenue and the group’s local operations saw revenue from this division increasing by only 3.9%.

Service revenue for the group showed a similar trend in terms of muted growth in South Africa (+2.1%) and strong growth (+15.6%) in Vodacom’s international operations. Roughly 74% of service revenue is derived from the group’s South African operations and 26% from the group’s offshore operations.

Vodacom’s dependence on the South African consumer will see future earnings impacted by the level of economic growth within the country and increasing competition in what is a saturated domestic market. In the mobile subscriber space, it’s becoming evident that Telkom has been increasing its local footprint at the detriment of the other major telecommunication providers.

Double digit earnings growth is expected to continue outside of South Africa but will not be enough to move the earnings needle for the group in the short to medium term. This is due to the relatively small revenue contribution international operations makes to the group’s overall earnings. Vodacom is currently bidding for a license in Ethiopia, which if successful, could aid earnings gains for the group longer term.

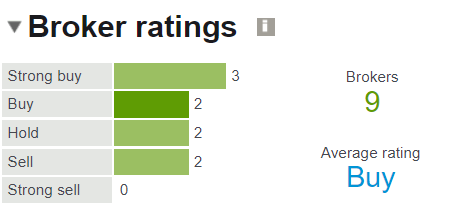

A Thomson Reuters poll of analyst ratings has a long term ‘buy’ recommendation on the stock.

Telkom: mobile subscriber growth strong, broadband underwhelming

H1 2020 results have shown Telkom’s group operating revenue to have increased by 4.7%, although EBITDA declined by 4.3% when compared to the prior year’s same six-month period.

The group has had an incredibly strong performance in the mobile division, growing its subscriber base by 75.7 % (vs H1 2019) to 11.5 million users, and increasing mobile service revenue by 56.6%. Telkom has had to increase its capital expenditure over the period by 66.1% to achieve this growth.

Where the group is not doing as well is in the company’s traditional business. Fixed voice and interconnect revenue declined by nearly 20%. The group has been looking to migrate its client base to new broadband technologies, such as fibre and LTE, although growth in this department has been insufficient in offsetting the losses stemming from the traditional business. Telkom has said that it will need 2 to 2.5 times more traffic in the newer technologies which trade at lower price points to offset the losses in the fixed broadband division.

Telkom is currently under cautionary as the company engages in negotiations on a potential acquisition which could materially affect the share price. Speculation has been rife that Telkom is revisiting conversations with Blue Label Telecoms on a possible bid for the ailing telecoms provider, Cell C. The Blue Label share price has reacted favourably to the rumours, which have now turned out to be fact. The potential acquisition is subject to Cell C reducing its leverage to more sustainable levels and the renegotiation of contracts more favourable to Telkom. Cell C is the third largest mobile operator in South Africa with 16 million customers. The company is currently indebted to the amount of nearly R9 billion. Telkom shares have come under enormous pressure in the short-term, expressing dismay at both the results and acquisition news.

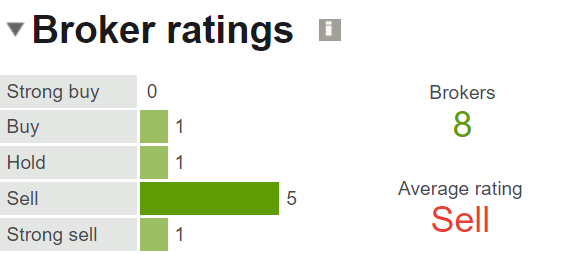

A Thomson Reuters poll of analyst ratings has a long term ‘sell’ recommendation on the stock.

MTN: double-digit growth

Q3 2019 results from the MTN Group have shown a double-digit increase (11.8%) in EBITDA, boosted by an increase in service revenue and improved operating margins. The group has managed to add 3.5 million new subscribers from the prior year’s comparative quarter. MTN’s results were aided by strong growth in its Nigerian and Ghanaian operations, although earnings growth in the domestic market remained muted.

In South Africa, MTN saw service revenue growth of just 0.4%, with overall subscribers falling by 300 000 to 28.9 million. As with other providers, this year’s ruling in March, by the communications regulator (ICASA) to reduce (out of bundle) data tariffs has weighed on earnings. The group has had to renegotiate a payment plan for Cell C relating to fees associated with roaming, which if accrued, would have lifted revenue growth to 3.5% for the quarter.

Of the locally listed telecoms providers, the MTN Group has the largest footprint outside of South Africa. Nigeria remains the groups largest source of EBITDA and is expected to deliver double-digit earnings growth over the next two years. The group’s geographical reach of earnings also provides it with the best exposure to the emerging consumer in Africa and the Middle East. While these jurisdictions (outside of South Africa) are expected to be levers for growth, geopolitical, regulatory and currency risk remain a catalyst for earnings volatility.

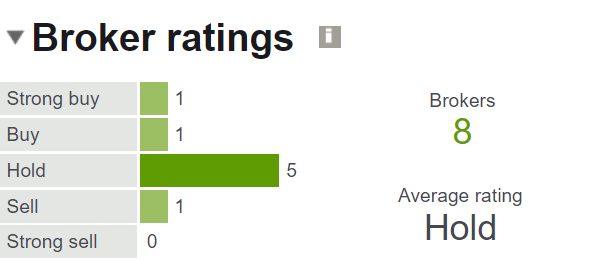

A Thomson Reuters poll of analyst ratings has a long term ‘hold’ recommendation on the stock.

For more market updates, visit IG.com DM

Author: Shaun Murison, Senior Market Analyst at IG