Kevin Brady, CEO of A2X. (Original photo: https://www.a2x.co.za/our-people/)

Kevin Brady, CEO of A2X. (Original photo: https://www.a2x.co.za/our-people/) Competing with an incumbent that has been a monopoly for more than 130 years was never going to be easy for South Africa’s alternative stock exchanges, but with the use of cutting-edge technology and an experienced executive team, Kevin Brady, CEO of A2X says his company has overcome many of the barriers to entry.

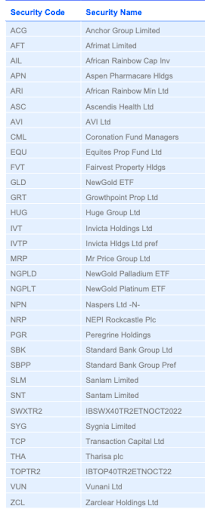

A2X has built up a kitty of about R2-trillion in market capitalisation and more than 29,000 trades since its launch in October 2017. Real estate investment trust (REIT) Fairvest Property was the bourse’s latest listing on 31 October 2019, bringing the number of represented issuers on the stock exchange to 32, as broken down in the table below.

So A2X is doing well and Brady expects things to get even better. But its choice in digital infrastructure might pay off more handsomely in the near future, which will make it great. That is if and when the Financial Markets Act aligns itself with international best practice, which Brady says seems to be the direction local regulators are moving towards. Overseas it is allowed to trade in primary listed shares on platforms other than the main bourse on which it is listed. That is not the case here.

They are called multi-trading facilities (MTF) in Europe and alternative trading systems in the US. But more on that later.

Meanwhile, the A2X stock exchange’s current modus operandi is simple. It is adding more liquidity to an existing local market by attracting secondary listings from issuers with primary floats on the JSE.

Brady says the A2X listing requirements reflect this. “No initial public offerings or capital raisings will be offered by A2X at this stage and once the business is up and running, additional products and geographical areas will be considered,” he says.

A major obstacle in the exchange’s endeavour to deepen the South African share trading pool, however, has been the country’s broker infrastructure, which until recently was incompatible with a multi-venue environment. Up to now, it has been the JSE way or the highway.

But many brokers have begun to re-engineer the way they work, Brady says, despite the challenges of integrating single-exchange legacy platforms into a modern eco-system, which remain.

They have seen the value in doing so “and have [also] realised the limitations of being tied to only one exchange,” he says.

A2x has partnered with a local technology firm to develop a post-trade platform, for this purpose. Post-trade processing occurs after a trade is complete. This is when a buyer and a seller compare trade details, approve the transaction, change records of ownership and arrange for the transfer of securities and cash.

This will make it both cost-effective and easy to trade client orders across both JSE and A2X market infrastructures, says Brady. “The system is being rolled out to selected brokers and is expected to be in full production by the first quarter of next year [2020].”

According to A2X calculations the savings in exchange fees and lower friction costs, which an alternative trading platform brings to market, as well as digital developments, can be up to 50%. These savings flow to the brokers and investors and are estimated to be upward of R1.2-billion a year, the company says, adding that it also improves the quality capital markets by narrowing spreads and improving liquidity.

The existing trading infrastructure, where the 30-odd secondary listings of A2X are conducting its business at present, is supplied by Aquis Technologies in the UK.

The core exchange platform includes a matching engine, surveillance system, as well as a bespoke clearing system, but more importantly, Aquis is authorised and regulated by Britain’s Financial Conduct Authority (FCA) to operate as a MTF.

By definition, and in essence, that is what A2X is. But as local laws stand, A2X is prohibited from doing what exchanges around the world can do.

SA’s Financial Markets Act (FMA) says that only an “exchange” can trade securities in the local market, and to qualify as such, a licence issued by the Financial Services Conduct Authority (FSCA) needs to be obtained.

Also, one can only trade in the securities of issuers with which a specific exchange has a contractual agreement. So you need permission from the Aspens and Afrimats of the world to be able to trade in their security — irrespective of the type of listing or share class, or where their primary listing resides.

For MTFs overseas it is all about leeway. You don’t even have to get on the highway. A consequence of MiFID II — a European Union directive regulating non-exchange financial trading (the US equivalents are known as alternative trading systems), platforms like Aquis, Turquoise and Cboe’s Bats can trade a wider variety of markets than most exchanges, including assets that may not have an official market, and in the securities of other exchanges. They don’t need the permission of the London Stock Exchange (LSE), for example, or that of its issuers for that matter. If a broker or investor wants them to be the middle-man in trades on BP or Vodaphone shares, they can.

That is the layman version. The book of jargon is thick and the testaments in technicalities are wide, but what is significant about MTFs in the local context, and for the purpose of this argument, is that if our regulations are amended to reflect that of the EU, it will make available to a secondary trading platform like A2X the entire JSE share pool without any paperwork required.

And as it is technically already an MTF by design, the transition will be, well, no transition at all. When it can call itself an MTF it can behave like one. An automatic venue for secondary trading.

Before the instructions of regulatory frameworks changed overseas, investors and brokers had to rely on national securities exchanges like Euronext or the LSE to be able to participate in capital markets, which is the situation South Africans find themselves in today. But faster transaction speeds, lower costs and trading incentives have helped MTFs become increasingly popular in Europe.

Another big difference in how business is conducted in many developed markets compared with SA is that locally a centralised regulatory model is applied, where exchanges are responsible for the behaviour of their own issuers. In the US, the Securities Exchange Commission, and in Britain, the FCA, run the show. The whole show, from beginning to end.

Brady foresees that when the FMA rules change, this sole centralised regulatory mandate will probably be pulled up to the level of the FSCA, but it will take time for the authority to build up the capability to be able to do so.

While that is happening, the bourses will probably continue to self-regulate, says Noah Greenhill, former head of the JSE’s AltX and now an independent consultant to many issuers, brokers and even some of the alternative exchanges.

“In SA we have multiple regulators, and the law states that each one of them need to have clear and specific listing requirements, by which their issuers have to comply, so there are a lot of details that have to be dealt with before any significant shift in approach will be possible,” says Greenhill.

But local authorities have not been blind to the benefits the global best practice has shown, nor have calls from industry for less friction fallen on deaf ears.

The 2018 Financial Markets Review was compiled by the South African Reserve Bank, FSCA and National Treasury to deal, among other things, with amendments to the FMA that will allow for MTF capability and a centralised regulatory framework.

The powers that be have consulted extensively with market participants since 2018 and Treasury has confirmed to Business Maverick that the 2019 update will be made available to the public before the end of the year.

So watch this space. Things are about to get quite interesting around here. BM