Steven Nathan, 10X Investments’ chief executive officer

Steven Nathan, 10X Investments’ chief executive officer

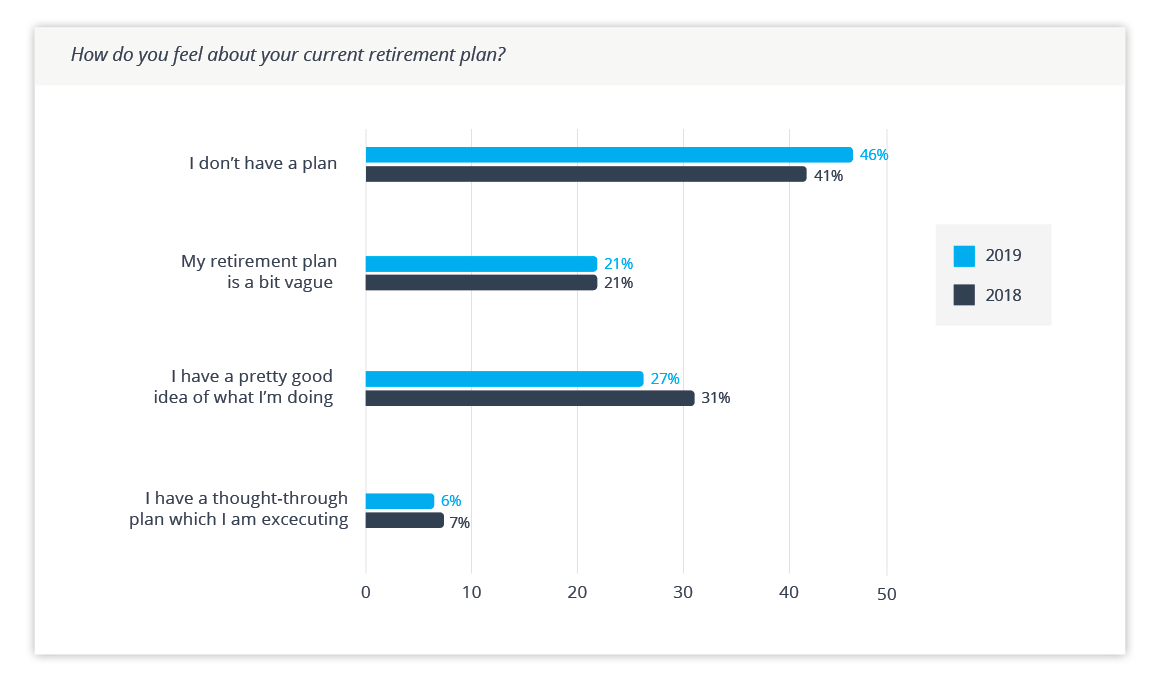

Almost half the respondents (46,2%) admitted they were not saving for retirement at all, with the overwhelming majority (91%) blaming insufficient means, or other priorities.

They are saying they can’t afford to save.

This should surprise no one. South Africa’s financial stress is palpable, manifesting not just in surveys like this, but in our rising national debt levels, the burden of insolvent state-owned enterprises (SOEs) such as SAA, Eskom and the SABC, the regular shortfall in tax revenues reported by Sars, and the many JSE-listed companies now reporting poor results.

Against this backdrop, it is understandable that many people are also struggling with their personal finances. And why our country’s household savings rate is effectively zero, one of the lowest in the world.

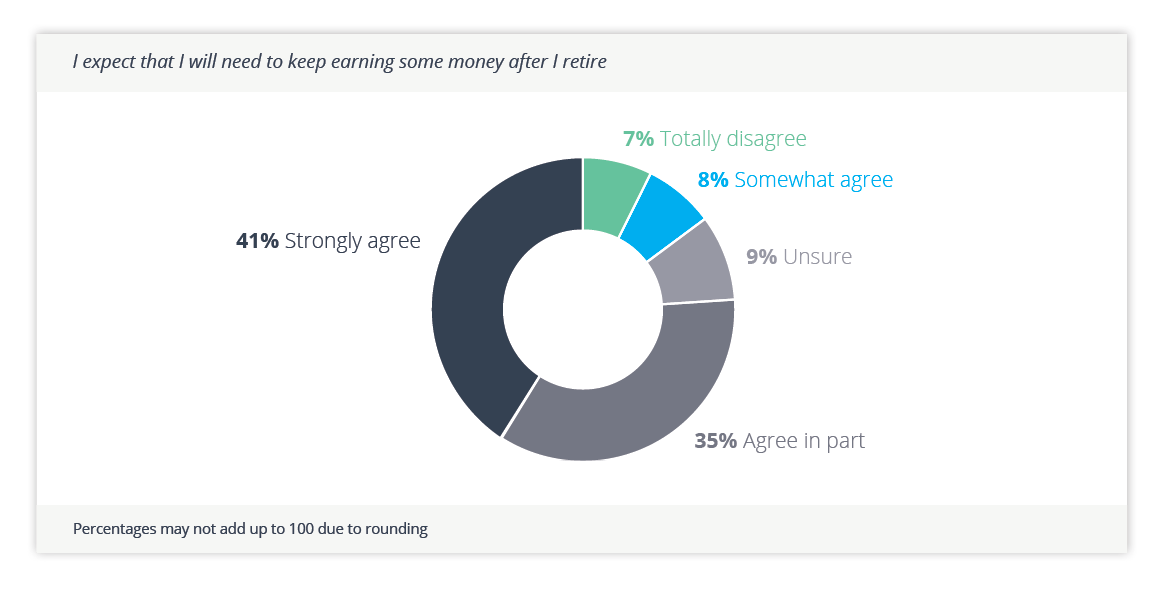

The report, which was released last month, found that even among those respondents who said they had some sort of retirement plan (roughly half), nearly 4 out of 5 accepted they would need to keep earning some income after they had retired. Others were planning not to retire at all. But how realistic is either expectation in a country with such a high unemployment rate as South Africa?

Unless we do something, the unemployment rate will only increase. Our population pyramid is pear-shaped, literally and figuratively, with 46% of South Africans are under the age of 25. If the current economic conditions persist most will struggle to find work. We are then facing an unemployment tsunami, with potentially dire social and political consequences.

This is our economic reality: we are caught in a vicious cycle of high unemployment, low growth, low saving and low investing. These factors reinforce each other. Unless we break the cycle, they will drag us into an even deeper mess.

The government has increased spending but has little to show for it other than ballooning debt, credit rating downgrades and a tarnished reputation. Something needs to change. Some commentators argue that now is not the time for austerity measures but staying on the current path would be doing more of the same while expecting a different outcome.

We cannot afford this path either.

If we can’t borrow and spend our way out of this hole our only alternative is to save and to invest. The two go hand in hand. Investments must be funded, and they cannot be funded by banks alone. The government lacks the capacity to raise much more debt and we cannot expect foreigners to bring their money here if we don’t also put our money where our mouth is. The private sector must come to the party, and so must personal savings.

The Chinese have posted the highest savings and investment rates over the past two decades. It is no coincidence that they have also had the world’s fastest-growing economy over this period. They have created hundreds of millions of jobs in this way because investment creates employment, which in turn drives spending and saving and more investment.

We need to build some of that momentum. Economic transformation is important, but for now we should prioritise participation over ownership. The best way to empower the average South African is to give them a decent education and create an economic environment that will give them the prospect of a decent job with decent pay. Only this will ultimately enable ordinary people to save, to invest, to own a share of the economy, and to build wealth.

We need to get the ball rolling, perhaps in the manner proposed by Finance Minister Mboweni’s economic growth reforms. He, too, posits that the only way out of our economic malaise is to raise investment levels. For that we need an environment that is conducive to capital spending.

What he says may not fully accord to ANC ideology but, in this case, the end surely justifies the means. He proposes lower barriers to entry in concentrated sectors, easier access to finance, less onerous regulation, curtailing state monopolies, encouraging small business development and, above all, providing a “stable macro-economic policy framework’” that instils confidence in the providers of capital. He lists many necessary initiatives that could support growth in other parts of the economy.

If this gets off the ground, the key will be funding. Is it a coincidence that President Cyril Ramaphosa recently broached the subject of prescribed assets in Parliament? Despite all the media noise on this subject, and speculation that it would simply mean more money flowing into non-profitable SOEs, government has yet to make any concrete policy proposals. But there has been much talk about getting pension funds to support infrastructure projects, which lines up broadly with the content of Mr Mboweni’s paper.

There is nothing wrong with this in concept, provided such projects come with the assurance of proper governance, the prospect of competitive returns and adequate liquidity to facilitate efficient trading and pricing. This calls for innovative solutions, but if these criteria are met, the pension industry would surely offer the necessary funding, even without prescription.

But this is a pipe dream if government plans to tap just existing retirement savings. Allocating 5% of a R3 trillion savings pool releases a once-off amount of ‘just’ R150bn. That sounds like a lot of money in absolute terms, but not so much when we consider Eskom’s R400 billion debt burden.

For a sustained impact on the economy we need to increase our overall household savings rate, if necessary, by making long-term saving compulsory for all employees. Again, this calls for innovative solutions. But if we are going to prescribe investments, it makes sense to also prescribe some form of saving, otherwise we run the risk of disincentivising those who are saving for retirement.

No doubt, a cry will go up that South Africans cannot afford to save. But given the desperate situation South Africa finds itself in, can we really afford not to? DM

*The annual Brand Atlas survey samples the universe of economically active South Africans (15,1m in 2019), defined by StatsSA as those with a monthly income in excess of R7,600 per month.

This article was written by Steven Nathan.

Steven Nathan is the Founder and Chief Executive Officer of 10X Investments. The disruptive asset manager released its second annual Retirement Reality Report this month. Click here for more information and a downloadable version of the report.

10X Investments is running a campaign to encourage South Africans to educate themselves about retirement saving. Everyone who engages with the campaign to discover what R1 million would be worth when they retire is entered into a draw and stands the chance of winning a R1 million 10X Retirement Annuity. https://www.10x.co.za/winthe10xmillion