Photo by David Mark on Pixabay

Photo by David Mark on Pixabay Just because an economic policy does not refer to macroeconomic policies does not mean it isn’t a macroeconomic policy.

We disagree with those who say “the problem with National Treasury’s economic policy document is that it is only about microeconomics”. True, the document does not explicitly refer to what most respectable economic policies address in the world today, namely the changes needed to monetary and fiscal policy in order to address the challenges of the day.

What it does refer to is “macroeconomic stabilisation”. Buried within that seemingly logical phrase is a bold claim: our macroeconomic framework is secure and tight, all we need to worry about now are the microeconomic details. This is the formulation that lies at the heart of all our economic policies since 1994. If this was an appropriate approach, why then are there more poor South Africans today than there were in 1994? Why do over 90% of all assets remain owned by 10% of the population? Why is unemployment just as bad today as it was in 1994? When it comes to economic policy, the only lesson we South Africans seem to learn is that we don’t learn from our mistakes.

What does “macroeconomic stabilisation” refer to? In essence, it refers to limiting the role of the state to ensuring that fiscal policy does not lead to the debt to GDP ratio rising above 60%. And it refers to the role of the SARB as the guarantor of a hawkish monetary policy that maintains the inflation target of around 4.5% no matter the consequences for employment levels. If these two numbers are fixed and non-negotiable, then yes, the cornerstones of macroeconomic policy are set. If macroeconomic policies cannot be discussed, then we only have microeconomic instruments to address our mega-challenges of unemployment, poverty and inequality.

But is this the only way to configure our economic policy framework? Why do we assume that the debt to GDP ratio should be 60% when no developed country has achieved economic development without going way above 60%? Why do we assume that an inflation target of 4.5% prevents runaway inflation when most of our inflation is caused by global market dynamics that affect the price of stuff we import, especially oil?

Reading the National Treasury document is like arriving in Havana: everyone drives cars from a bygone era because Cuba was isolated by the US blockade. National Treasury drives a general equilibrium model from a bygone era. Both result in cognitive dissonance. Somehow National Treasury did not notice that in the (northern) summer of 2016, the high priests of economic policy declared that general equilibrium models that everyone uses are no longer useful.

Paul Romer, Nobel Prize winner for economics and Chief Economist of the World Bank at the time, wrote a paper (that lost him his job) where he declared, “For more than three decades, macroeconomics has gone backwards… .”1

Olivier Blanchard, in a paper he wrote a month after resigning as Chief Economist of the IMF, said, “I see the current DSGE models as seriously flawed …. .”2

Narayana Kocherlakota, Rochester University Professor of Economics and former President of the Federal Reserve Bank of Minneapolis, declared, “…we simply do not have a settled successful theory of the macroeconomy. The choices made 25-40 years ago – made then for a number of excellent reasons – should not be treated as written in stone or even in pen.”3

These statements from the high priests of mainstream economics are the equivalent of the pope renouncing Catholicism. And yet, reading the National Treasury document, one wonders if the National Treasury has read these papers? And if so, would it not be more honest to open up the general equilibrium model for public scrutiny? And we all need to ask whether there is an alternative non-equilibrium model that may generate more contextually appropriate results?

During the post-World War II era until the 1980s, mainstream Keynesian economics was premised on the assumption that fiscal policy must be used to stimulate investment during recessionary times (increased spend and/or lower taxes) supported by monetary policy (lower interest rates), and during growth times fiscal policy must reduce investment (less public spending and/or higher taxes) and save supported by monetary policy (higher interest rates). The underlying assumption was that economies tend towards disequilibrium and therefore state intervention is rational.

This consensus was shattered by the rise of the neoliberals who argued that the fiscal crisis of the state after the oil crisis of the early 1970s must be resolved by shrinking the state, limiting fiscal spending, prioritising inflation targeting using monetary policy and balancing budgets (i.e. limiting debt).

Armed with the new computing power delivered by the information technology revolution, elaborate extremely elegant mathematical general equilibrium models were built and installed by World Bank and IMF teams into the beating heart of economic policymaking in governments across the world. These “pacemakers” resulted in a kind of intellectual monocropping that allowed economists to abstract out everything about the real economy that really mattered (in particular the declining energy returns on energy invested since the 1990s).

Debate, of course, became non-essential. This Nintendo generation of econometricians gained enormous power and prestige. The end result was the financialisation of the global economy, a shift from investment-led inclusive growth over a sustained period of time to debt-funded consumer-driven volatile economic growth. Meantime, the state-driven Chinese economy became the world’s producer. As banks were deregulated, the money they issued as debt massively expanded the total quantity of cash available to drive a consumer boom that made everyone think that depression was a thing of the past.

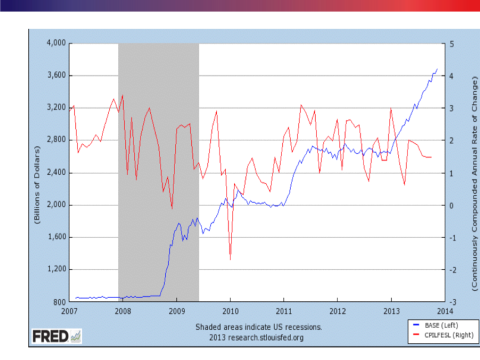

Economists claim that data matters. While we both know that the only way a bad theory is replaced is when a better theory comes along, let’s take a look at the data. Take the relationship between money supply and inflation. For neoliberals, increasing money supply should trigger inflation. This never happened. The graph shows what happened in the US economy: an increase in money supply as a result of Quantitative Easing (2008, 2011 and 2013) resulted in inflation that is essentially flat (if you remove the volatility).

In orthodox models, if public debt goes up, so should the spread on treasury bonds (i.e. less demand for them pushes up the interest rate to compensate for the risk). This also did not happen. The graph shows a substantial increase in public debt in the US economy between 2005 and 2014 (itself contrary to what neo-liberals would have preferred), but the spread in the ten year Treasury bond generally declined.

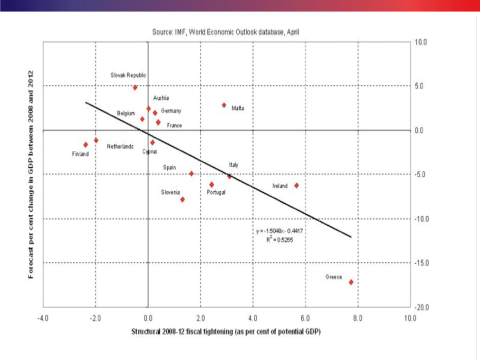

According to GE models and following the anti-Keynesianism of renowned economist Alberta Alesina (whose models were later proven to be wrong), fiscal contraction should lead to economic recovery because more space is created for private sector investment. In reality, this did not happen. The table shows that during the period of fiscal tightening between 2008 and 2012, the opposite happened. According to this IMF data, the more fiscal austerity there was, the lower the growth rate, with Greece being the poster child of this fantasy.

National Treasury has launched a new austerity drive despite the call by an ex-Treasury official to do the opposite4.

Even mainstream economists who are essentially neo-liberals but influenced by Keynesian thinking have broken away from Alesina’s misguided notion of “contractionary expansion”. Leading economists like Larry Summers, Olivier Blanchard and Jason Furman are all calling for a return to expansionary fiscal policies precisely because the evidence now shows this “sucks in” rather than “pushes out” private sector investment. Again, is National Treasury hearing this?

So there is an alternative and it comes from so-called heterodox economists. The starting point is a shift from the supply side to demand-side economic policy thinking. Underpinning this is an acceptance that economies tend towards disequilibrium, and therefore state-led directionality and intervention is a necessity. The focus would be aggregate demand, employment creation, and inflation targeting would be subordinated to wider economic goals. Fiscal policy would lead and monetary policy would support macro-economic goals. Investment levels would be the primary focus and measurement of progress would not be GDP per capita, but overall wellbeing (following the lead set by New Zealand).

In this configuration, the state’s role as a driver of development – via, in particular, the development finance institutions – would become a reality. A new generation of coordinated institutional arrangements would be established to coordinate the deployment and allocation of public and private capital towards building and supporting a productive, innovative economy and a revitalised socio-economic infrastructure.

This way of derisking investment holds the key to ending the private sector investment strike that persists despite words to the contrary at the Investment Summit. To respond to this by saying savings levels are too low to sustain investment-led growth is to totally miss the point. Banks create money by issuing debt. When this goes into consumption and not production, that is when things go wrong. The state has the instruments to intervene to direct the flow of investment.

This approach would require the adequate regulation of domestic finance and management of cross-border economic flows. It would require reshaping and reforming financial markets to move away from high short-term returns and the maximisation of shareholder value that requires them to behave speculatively and exploitatively in domestic markets. Instead, the focus would be on the building of financial markets that serve the country’s socio-economic developmental goals.

This alternative approach would require increased government spending and rising debt to GDP ratios to support industrial policy and the improvement of the outcomes in the education and health sectors. To prevent these funds from being depleted through rent seeking, ring-fenced institutional arrangements that blend public and private funding will be required. This will ensure that funding achieves the desired goals.

The entire macroeconomic literature has no compelling evidence on what the debt to GDP ratio should be. The famous Reinhart and Rogoff paper on this subject5 said that it was only at levels of debt to GDP above 90% that a negative impact on GDP growth appears. Even though the datawork in this paper was thoroughly discredited, the consensus now is that there is no universal threshold applicable to all contexts – if anything, it is higher than 90%.

Only three of the G7 countries are below 90% (Canada, UK and Germany), and none are below 60% (with Germany only coming close). In the most advanced models today, at least three other variables influence public debt levels: the employment rate, the labour share (of the GDP) and the private debt/GDP ratio. From this perspective, the inflation-focussed National Treasury model is crude and totally inappropriate for the SA context.

Ultimately, we need to face a simple reality: given our realities, and given that austerity will not stimulate growth under these circumstances, why must monetary and fiscal policy remain sacrosanct, and therefore non-negotiable? No country achieved its development targets with low inflation and a 60% debt to GDP ratio. Why do we think we can do it? And what have we got to fear? If savings are low and we want to end the investment strike, why not increase debt to stimulate growth in ways that will make it possible to pay off the debt? Surely the alternative is worse: rising debt levels to mitigate the consequences of low growth in a high unemployment environment to stave off a revolution.

Given our challenges, the important question is not the size of the fiscal multiplier (i.e. spending to GDP growth ratio), but how the fiscal multiplier becomes a policy variable for determining how government should spend and invest. This means doing the calculations as to what investments will generate the best returns (financial, as well as developmental).

And here there is much in the National Treasury document that is useful. For example, the emphasis on removing restrictions on renewable energy in the IRP and no mention of nuclear is an obvious case in point: the returns on renewable energy investments are obvious now that it costs 60c/KWh compared to coal at R1.05 c/KWh. These new methods for assessing the socio-economic and environmental impact of blended public and private sector investments will shape the way institutions are configured to limit rent-seeking. The role of the DFIs – the IDC, DBSA, Land Bank and NEF – will be key.

In short, microeconomic interventions cannot work if the macro-economic framework is non-aligned with what is required. By only focussing on micro-economic strategies, we may well be unwittingly endorsing intellectually indefensible and developmentally irrational macro-economic assumptions. DM

Prof Mark Swilling, Centre for Complex Systems in Transition, Stellenbosch University

Prof Gael Giraud, Ecole Nationale des Ponts et Chaussées (ENPC), Paris, former Chief Economist of the French Development Bank, and Extra-Ordinary Professor, Stellenbosch University

1. Romer, P. 2016. The trouble with macroeconomics. Delivered January 5, 2016 as the Commons Memorial Lecture of the Omicron Delta Epsilon Society.

2. Blanchard, O. 2016. Do DSGE models have a future? Washington, D.C.: Peterson Institute for International Economics, Policy Brief.

3. Kocherlakota, N. 2016. Fragility of Purely Real Macroeconomic Models. Cambridge, MA: National Bureau of Economic Research, NBER Working Paper No. 21866.

4. Wilcox, O. 2019. There is no fiscal problem in SA. Power Business, 26 August 2019.

5. Reinhard, C. & Rogoff, K.S. 2011. Growth in a time of debt. Cambridge, MA: National Bureau of Economic Research. Working Paper No. 15639.