One of my childhood memories is of sitting in my grandparents’ lounge watching a slide-show on a Kodak projector. With lights dimmed and curtains drawn, my grandfather flicked through the cartridge of slides projected on to their living room wall.

The pictures included some of their holiday trips to various parts of our beautiful continent, and one in particular, that of the construction of the Kariba dam more than 60 years ago, is indelibly printed in my mind.

Having personally visited the dam a few times, the sheer scale of the wall and how much water it holds back to form Lake Kariba – the world’s largest reservoir – is impressive on a grand scale. This engineering marvel also allowed for the efficient generation of renewable hydroelectric power for the region. But its 60th anniversary since completion has been marred by the impact of droughts and uncharacteristic weather patterns, resulting in a dramatic reduction in the power it’s able to produce, leaving millions in the dark.

This story has a number of parallels to our investments and savings today, and the lack of returns we are now experiencing from the mainstay of growth in most of our portfolios – our local equity market. Over the past five years, the majority of equity funds haven’t managed to keep pace with inflation1, resulting in a palpable sense of despair and anguish about our financial well-being and whether long-held assumptions about investing still hold true.

Against this backdrop, a global mega-trend to greater adoption of lower cost and more efficient index-based investment strategies, commonly referred to as passive, has been playing out. Globally the money which is flowing out of traditional, actively managed mutual funds isn’t all flowing into vanilla index funds. Some of it is making its way into smart beta or factor index funds. These flows have been driven by disappointing active management returns, cost sensitivity and the proven track record of grouping stocks together which exhibit specific characteristics, thereby improving performance and managing risk over time. This is by no means a flash in the pan. According to BlackRock, globally the factor industry is estimated to be $1.9-trillion in size and is projected to grow to $3.4-trillion by 2022.

What is factor investing?

Factor investing targets specific performance drivers shown to have delivered excess returns over time. These factors are intuitive, well understood and measurable investment ideas which explain stock behaviours. Stocks which exhibit these factors are identified and grouped together in order to achieve a predefined goal. These goals are critical and may include generating above-market returns, reducing risk or enhancing diversification. These performance drivers or factors are underpinned by sound theoretical and economic principles which ensure factors continue to deliver into the future.

Furthermore, smart beta (factor investing in index form), is rules-based and systematic in nature, providing investors with greater transparency and lower governance oversight, offering greater peace of mind that what you’ve invested in remains true to label and continues to behave as expected.

This approach is different to traditional active investing, where a broad philosophy or style typically governs the investment decision-making process, but because there is subjectivity involved, it can lead to unpredictable results or managers delivering portfolios that may seem contrary to their stated investment philosophy – also known as style drift. This becomes particularly challenging and problematic when trying to combine different managers’ funds to reduce risk, only to discover some of them may be making very similar, yet unintended types of investments.

The pillars of equity factor investing are value, size, momentum, quality, low volatility and yield.

The value factor aims to capture excess returns from stocks that have low prices relative to their fundamental value. This is commonly tracked by price to book, price to earnings, dividends, and free cash flow. Companies that exhibit value characteristics typically face economic headwinds to their business and may have large capital investments that are not easily resized to adapt to these unfavourable conditions. They, therefore, trade at discounts to their fundamentals and potential, which is what offers the premium for those investors who can afford to be patient.

The quality factor captures companies that are typically more expensive than their value peers, for the very reason they are able to withstand economic downturns better. Quality companies tend to be more conservative businesses and are characterised by higher and more reliable profits through time.

The momentum factor is often mercurial in that it will overlap and capture whichever other factor or theme happens to be paying off at the time. Stocks that have outperformed in the past tend to exhibit strong returns going forward as investors take time to digest the impact of changes to a business and extrapolate these into the future. Momentum is one of the strongest factors in the South Africa context, but it requires very active – albeit systematic – management for it to be harvested correctly.

Our research confirms that factors deliver excess returns over long periods of time relative to our local equity market.

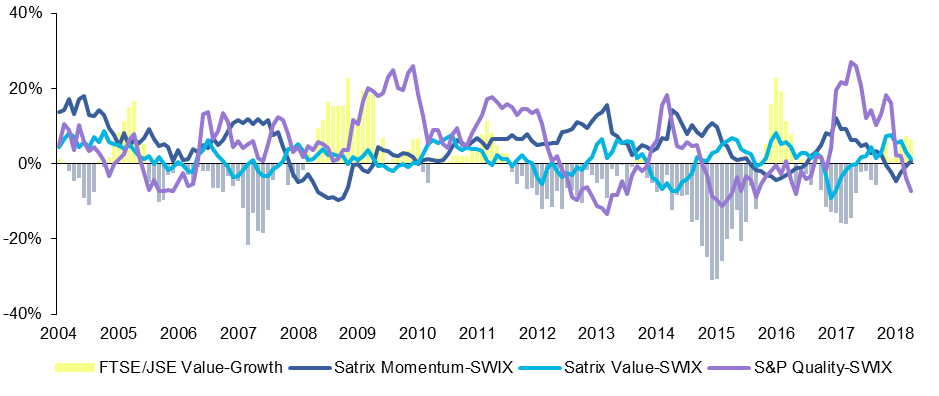

Excess factor returns in South African equities

/file/dailymaverick/wp-content/uploads/BM-Kingsley-Williams-opinionista-Factor-Investing-image4.png "(supplied)")

Source: Satrix

However, the cyclical nature of factors also includes periods of underperformance relative to the market – a phenomenon value investors have been well acquainted with and which bears striking similarities with the wild weather patterns inhibiting the power produced by the Kariba dam.

The cyclical nature of factors is depicted in Figure 1, where the bars indicate whether we are in a value or growth cycle. Yellow bars indicate we are in a value cycle, whereas grey bars indicate we are in a growth cycle. The lines represent whether a particular factor index is outperforming the market on a rolling 12-month basis.

Figure 1: Factor Indices – Rolling 1-year excess returns

Source: FTSE/JSE, S&P & Satrix

The navy line indicates the momentum index relative to the market. Momentum tends to do well when a value is underperforming, but can face headwinds when the market is in a value cycle.

The turquoise line is the value index relative to the market, which as expected pays off when value outperforms growth. Momentum and value naturally complement each other within a portfolio as they pay off at different times.

The purple line represents quality’s performance relative to the market, which isn’t explained as easily through a value/growth lens, but you’ll see it also pays off at different times to both value and momentum, particularly during periods when they may not be delivering as much, such as 2009, 2010 and 2017. Quality, therefore, adds further diversification to a portfolio.

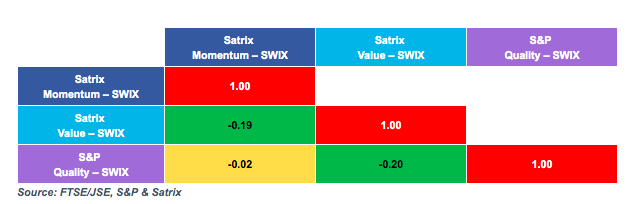

Investing in multiple factors makes sense because while individual factors each offer a premium to the market over long periods of time, they also carry the risk of shorter-term cyclical underperformance. Blending multiple factors together mitigates this risk precisely because they pay off at different times as confirmed by the negative or near zero correlations of excess returns amongst our preferred factors of momentum, value and quality in Table 2 below.

Table 2: Correlations of 1-year excess returns

Source: FTSE/JSE, S&P & Satrix

How to combine factors

Single-factor funds are useful for clients wanting greater control in the construction of their broader portfolios or to complement their traditional actively managed funds with factors that may be missing.

Alternatively, instead of blending multiple single-factor funds together, a combination of factors can be blended at stock level and delivered in a single multi-factor fund. This multi-factor approach at stock level has the advantage of enhancing the exposure to the desired factors while at the same time managing risk at a broader level.

The recently launched Satrix SmartCore™ Index Fund provides multi-factor exposure to value, quality and momentum in a single equity unit trust, and is the same equity strategy that has underpinned the Satrix Balanced Index Fund.

While those dependent on the reduced electricity output from the Kariba dam are having to grapple with where they will source power, investors are similarly faced with equity market returns that haven’t contributed to growing wealth over the last five years. However, when blending factors together, your portfolio becomes more resilient to changing market conditions, and not reliant on only one source of returns or style of investing, thereby giving you a better chance of achieving your financial goals.

Over the last five years and within a tough market environment the Satrix single factor funds delivered exemplary performance relative to the General Equity category. BM

Kingsley Williams is the chief investment officer at Satrix

Correction: Graphic designations corrected.