Naspers announced on Monday it would be hitching a ride to Amsterdam to list on the Euronext exchange, listing all its international assets in Europe in a company that would still be controlled by JSE-Listed Naspers.

The magnitude of the announcement and the “meh” reaction by the stock market in a way summarises an odd mixture of characteristics so typical of the complicated beast that is SA’s most valuable locally listed company.

What the company announced specifically was that it would list on Euronext in Amsterdam another company called Newco, which would contain all but a few tiny SA assets, and it would consist of effectively 25% of its existing share register. In other words, no new money is being raised, and existing shareholders are not being diluted.

Once the dust settles, the result will be that the local company Naspers will own 75% of Newco. The crucial control structure, of which existing chairman Koos Bekker is the most notable member, that gives a few insiders 66% control over Naspers will be replicated in the Dutch company.

The result is that instead of a two-level pyramid, we now have a three-layer pyramid. So why is this a good thing?

The big problem, about which investors are painfully aware, is that Naspers owns 31.2% of Chinese internet giant Tencent, which it acquired for $36 million in 2001, something that was easily the best buy of the century. That stake is worth $134bn which dwarfs Naspers’ market capitalisation of around $99bn.

One way of understanding this oddity is that the market is valuing everything other than the stake in Tencent as worth minus-$35bn. That’s an enormous number of dollars to be minus, even in 2019.

The other way of looking at the problem is in some ways more likely; Chinese investors in Tencent have had a terrible rush of blood to the head, something that occasionally happens on stock markets, and they are massively overvaluing Tencent. You take your pick.

The company’s solution to this problem - the kind of problem by the way that everyone on the planet would want - is to try and increase the liquidity of the share, and that means trying to create more buyers.

The company demonstrated the problem at the presentation on Monday by showing a graph of the value of the company and its proportion of the SWIX (the Shareholder Weighted Index, the big daddy of the JSE’s indexes). What this was intended to show is that the closer the company got to be a quarter of the index - the maximum any one counter can be - the more sellers emerged.

In other words, as Naspers got closer to this ceiling level, some shareholders were forced to sell so that their weightings matched the index. This rule was effectively in Nasper’s case driving negative investor behaviour, said Old Mutual Equities analyst Philip Short.

There are also some of the typical problems associated with investing in SA: rand exposure and political risk.

"The listing will present an appealing new opportunity for international tech investors to have access to our unique portfolio of international internet assets," said Naspers Chief Executive Bob van Dijk.

Listing in Amsterdam has some distinct advantages. It’s coincidentally Van Dijk home, not that any executive would make hugely significant decisions based on their personal comforts.

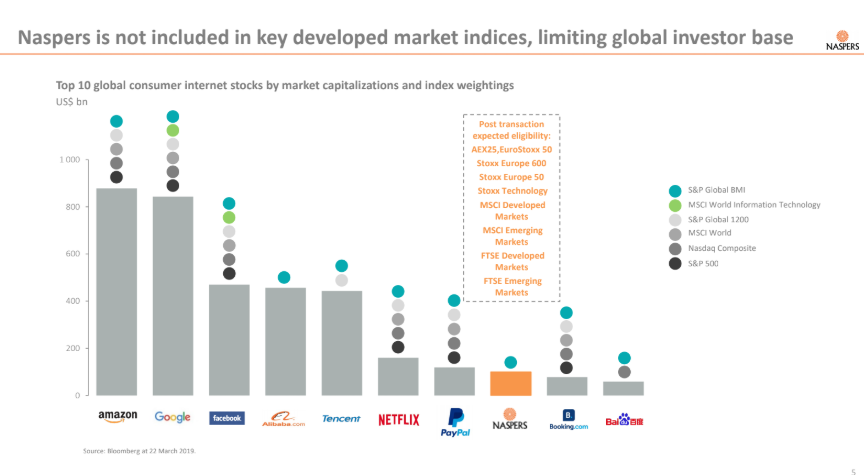

One real advantage would be that Newco would be right up there with some of the biggest listings on the exchange, which would help expand the investor base, partly by being a member of a whole host of European indexes.

The idea did get the thumbs up from local fund managers, even though it does imply, yet again, a company edging slowly away from SA. “Let the grasshopper jump away and run free,” said Vestact fund manager Bright Khumalo. Naspers has just become too big for SA, he said.

It will cost the company a bit: the company already claims it is committed to spending R3.2bn to support SA technology entrepreneurs develop and they are now going to add R1.4bn to that number over 3 years.

So why not list more than 25% in Europe? The answer is that over 30% would create a big “tax event”. What about unbundling Tencent? That too would have created a “tax event”. Hmm.

Short says he has a sense that this is not the end of the road in the restructuring process. As some of the investment areas of Naspers start to really come to fruition, they might be listed in Amsterdam too, somewhat in the same way Naspers listed its DSTV assets on the JSE.

Others are more direct. “This listing is patient and concerted effort to rebase SA’s largest company by market cap into Europe and ultimately exit South Africa,” said one.

So if this is all a brand new attempt at realising shareholder value, why did the share price not move? Actually, it did move a bit: it went down 1.6%. Surely, that wasn’t supposed to happen?

It was dragged down a bit by Tencent trading lower in Europe, but still.

Short is philosophical about it. “We will have to see what value trading does take place,” he said, pointing out that the creation of the new company is some time off.

Yet, it’s possible too that shareholders were looking for something a bit more revolutionary than evolutionary.

Comments

Scroll down to load comments...