South Africa

Analysis: Zen and the art of municipal finance figures

The fourth quarter’s municipal finance figures were released on Friday. PAUL BERKOWITZ looked at of the numbers and found some of the accounting very creative indeed. It looks like the art (and artfulness) of municipal officials are trumping the science of national treasury.

On Friday, the national treasury released the latest Section 71 (quarterly municipal finance) figures. These figures refer to the final quarter of the 2011/2012 municipal financial year, covering the period from April to June 2012.

In a previous article we described some of the problems experienced in local government financial reporting and management. The biggest problem appears to be a lack of consequence for municipal departments that fail to follow the law. There is growing evidence of a culture of impunity.

The latest quarterly release deepens the suspicion that financial management is not improving in municipalities, and that financial officers feel the legal framework is open to interpretation. The same problems identified in earlier quarters continue to affect municipalities and there are one or two new ones that have come to light. The analysis in this article focuses on the eight metro municipalities. The same problems identified in the metros are evident in the other municipalities, except that they’re more pronounced.

Firstly, municipalities are still struggling to both raise and spend all of their budgets, particularly their capital budgets. The metros were quite successful at meeting their operating revenue targets – all except Mangaung (91.4%) were within 4% of their targets. In terms of meeting expenditure targets for the operating budget, the results were slightly less sterling. Only four metros spent over 95% of their budget (Johannesburg, Nelson Mandela Bay, Tshwane and Ekurhuleni). Buffalo City spent just 83% of its budget and Manguang just 78.9%.

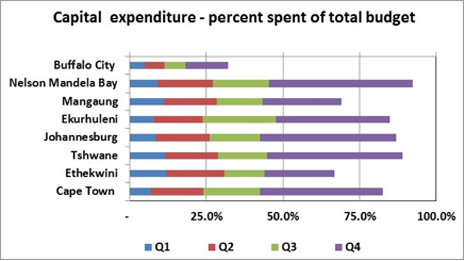

The spending of the capital budget is much worse. Three of the metros spent less than 75% of their budgets. Buffalo City was the worst of all, managing to spend just 32% of its budget. The table below summarises the capital spending in the metros:

Another continuing, disturbing trend in capital expenditure is the underspending in the first three quarters of the year and the big race to catch up in the final quarter. All of the metros had spent less than 50% of their budgets by the three-quarter mark, and half of them spent upwards of 40% of their annual budgets in the last quarter.

There are a couple of legitimate reasons for the underspending, including the mismatch between the national and local government financial cycles, but a lack of project management skills in the municipalities is also a factor. The municipal infrastructure grant (MIG) is a conditional, ‘use it or lose it’ grant which explains the mad rush to spend the budget at the end of the year. One obvious concern is the quality of the decision-making that goes into the end-of-year spending spree.

A new phenomenon, related to the underspending, has been identified in this quarter, and that is the last-minute adjustment of budgets to downplay the degree of underspending that is going on.

The legislation (specifically the Municipal Systems Act) allows for a municipality to table an adjusted budget. There are a number of circumstances under which a municipality can adjust its budget, but the most common reason is to reflect the change in allocations from national government following the release of treasury’s mini-budget. The release for the third quarter of the municipal financial year typically contains an adjusted budget for all municipalities.

In this fourth quarter release, a sizeable chunk of the municipalities have included a second adjusted budget, which is unusual. Of the eight metros, three adjusted their operating budgets for a second time and two adjusted their capital budgets. The City of Cape Town adjusted both its operating and capital budgets in the fourth quarter, although the magnitude of adjustment was relatively small.

In BCM, the original operating expenditure budget for the year was R3.6bn, which was adjusted downward at mid-year to R3.4bn. This reduction of some R200m was cut from the ‘other expenditure’ line item. The third quarter report from Treasury reflected the adjusted budget.

The fourth quarter report from Treasury shows that the adjusted budget for operational expenditure is R3.7bn, R100m more than the original budget and R300m more than the first adjusted budget. Once again, virtually all of the adjustment in expenditure comes from ‘other expenditure’.

There may have been legitimate reasons for this second adjustment, but it looks suspicious. When officials in the treasury were asked about this trend, they confirmed that some municipalities over-estimate their budgets, particularly for revenue, at the start of the financial year. They then adjust their budgets down at the end of the year to correct their initial overshooting.

A similar development was seen with the capital budget (revenue and expenditure) for Nelson Mandela Bay. In the third quarter of the financial year, the adjustment budget was given as unchanged from the original budget (R1.4bn in both cases). In this latest fourth quarter release, the adjusted budget is given as R1.2bn. Some R200m (or almost 15%) of the budget has been shaved in the final quarter.

This downward adjustment allowed the municipality to reflect capital spending of 96.1%. If the adjustment hadn’t been made, the municipality would have spent only 84% of the capital budget.

The practice may not be illegal, but it is highly unprofessional. It also makes a mockery of the principles of sound financial planning. It whittles away the incentive for finance departments to plan carefully and to achieve greater accuracy in budgeting in an iterative way. Why should a municipality put effort into financial planning when the spending and revenue targets can be changed after the fact?

Apart from the growing popularity of this creative accounting, the metros seem to have stabilised their debtors books, at least for the quarter. The obvious exception is the City of Johannesburg, whose debtors book grew from R14.3bn to R15.2bn. Most of the new debt is younger than 30 days, which is a bit of a relief, although there’s not too much that’s pretty about a 6% increase in the debtors book in one quarter.

The general impression from these latest numbers is that municipalities have not properly wrestled with the shortcomings in their accounting practices. Rather than budget properly from the beginning – measuring twice and cutting once, as it were – they are happy to adjust their targets to fit the facts on the ground. They can do this safe in the knowledge that there are no penalties for not doing the job properly in the first place. Municipal government has become a giant Stygian stable, and government officials have become so used to the smell that they’re surprised we find it offensive. DM